As automated valuation models (AVMs) have become more commonplace, appearing everywhere from professional real estate brokerage websites to consumer-facing portals, the biggest drawback of using technology to generate a home value has become clear: AVMs can’t see the property. It’s impossible for an algorithm to know whether a home has been impeccably maintained — or whether broken windows and sagging porches indicate that it’s dilapidated and needs extensive work.

The best way to determine a home’s condition is to send a human to examine the home. Appraisers have traditionally completed this in-person task, and that process works well when full appraisals are required and can be obtained in an affordable, efficient manner for each and every home that needs one … not just for a sales transaction, but for home equity loans and lines of credit (HELOCs), loan modifications, second mortgages, refinancing, and many other loan and financial activities.

But when a full appraisal is not required to support a financial transaction, and assessing homes for all these different loan and financial needs with a full appraisal is expensive and takes days (or sometimes weeks); then lenders, servicers, traders, and portfolio managers often seek alternative solutions that satisfy their requirements while saving time and money.

Now there’s an alternative: the HouseCanary Agile Evaluation (formerly known as HouseCanary Value Report + Inspection).

What is the HouseCanary Agile Evaluation?

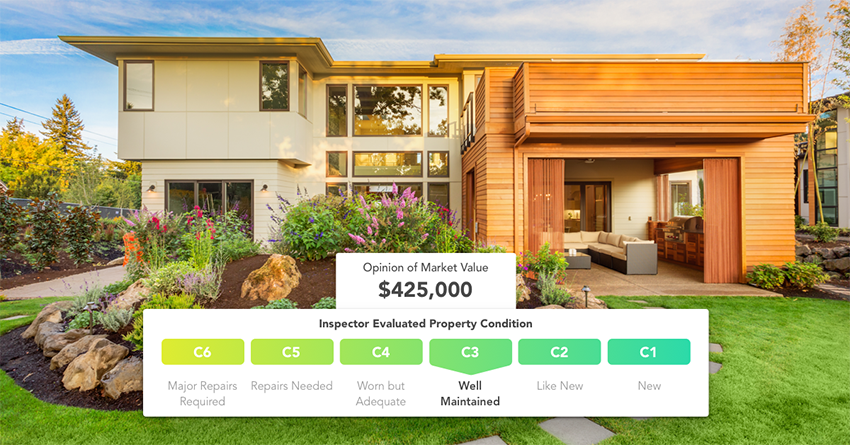

The HouseCanary Agile Evaluation is a residential evaluation report. It’s a condition-informed valuation report that uses both the technological advantages of an AVM and the in-person expertise of a human who can document and report the home’s condition. It qualifies as a sufficient home valuation product under the de minimis guidelines in the Interagency Appraisal and Evaluation Guidelines (IAG Guidelines), which means that it can be used as a compliant valuation solution for transactions under $250,000.

When the condition information is incorporated into the home value report, HouseCanary’s proprietary algorithms and deep real estate data are also able to calculate whether that condition is better or worse than the other homes on the block and in the surrounding neighborhood. We know the percentage difference between a poor-quality and average-quality home is likely not the same as the difference between an above-average and excellent-quality home. And we apply those differences to each home’s valuation so we can understand how condition is affecting the home’s fair-market value.

Between the deep data and the human documentation of condition, our Agile Evaluation is a worthy option to support home equity lending or as a replacement for a broker price opinion (BPO).

How can you use a residential evaluation report?

According to the IAG Guidelines, which were established by five financial agencies in 2010, residential evaluation reports can be used for:

- Loan originations and transactions for homes less than $250,000

- HELOCs

- Default servicing

- Whole loan trades

- Portfolio refreshes

- Loan modifications

- Bank regulator requirements

- Second mortgages

- Refinancing

- Home equity reviews

- Balloon loans

- Replacing BPOs

Accounting for condition with thorough, boots-on-the-ground human inspections eliminates the traditional AVM blind spot, generating a compliant and data-backed valuation that can be used in a variety of ways.